Risk-adjusted return measures for selecting optimal mutual fund investment portfolios

(1) Adlai E. Stevenson High School

https://doi.org/10.59720/24-016

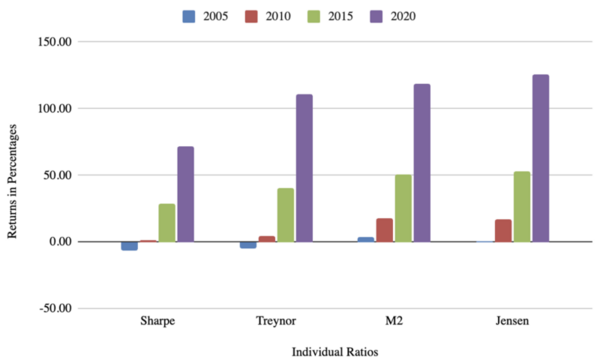

Investing has become an increasingly popular way to generate passive income. The purpose of this study was to determine which combination of the risk-adjusted return measures of Sharpe ratio, Treynor ratio, M2 measure, and Jensen’s alpha would provide the investor with the optimal investment portfolio of mutual funds to maximize returns. Using data from 1995 onwards, mutual funds were compared against the Dow Jones Industrial Average to evaluate relative performance. We hypothesized that the portfolio would perform better as more risk-adjusted return measures were used in conjunction because each individual measure already attempts to find the best mutual funds to use for the investor. Therefore, by combining various measures, there would be a multitude of supposed best performers that would provide greater returns. The results indicated that for shorter timeframes of 5 and 10 years, the M2 measure delivered the highest returns of 3.65% and 17.78%, respectively. Over longer periods of 15 and 20 years, Jensen’s Alpha outperformed, with returns of 52.57% and 125.38%, respectively. However, for more risk-averse investors, the combination of M2 and Jensen’s benefited from 116.12% returns and a larger number of funds, increasing diversification for slightly less profits. This study highlights the value of testing and refining the methods used to evaluate investments. By demonstrating that some measures excel in specific timeframes or risk preferences, it encourages investors to critically assess and adapt their strategies. offering a framework for informed decision-making in an unpredictable market, thus benefiting both individual and institutional investors.

This article has been tagged with: