Sector Dynamics: Equity and fixed-income performance across market cycles

(1) Mary Institute and St. Louis Country Day School, (2) University of Chicago Booth School of Business

https://doi.org/10.59720/25-069

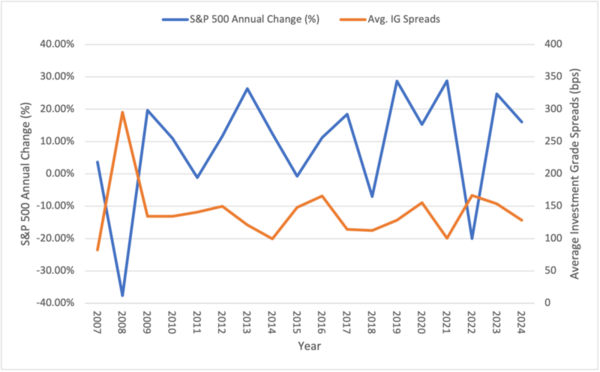

Investment decisions require balancing risk and return, which is a core principle of Modern Portfolio Theory. Understanding how different asset classes interact is essential for building resilient portfolios, especially as equity and fixed-income markets respond differently to economic conditions. We delve into the performance of the Standard and Poor’s (S&P) 500 Information Technology and Financials equity sectors compared to their corresponding U.S. investment-grade fixed-income returns. Correlations were evaluated between sector returns and critical metrics such as price-to-earnings ratio, credit spreads, and government debt yields. Using data from 1995 to 2025, we analyzed the role of diversification in portfolio construction through Modern Portfolio Theory. We hypothesized that there would be measurable and negative correlations between S&P 500 equity sector returns and their corresponding investment-grade fixed-income spreads, and that these relationships would vary in strength across recession and expansion periods. Our results revealed notable relationships between equity and fixed-income performance across various economic cycles, emphasizing the importance of sector-specific strategies in managing risk. This analysis questions traditional views on the stability of investment-grade bonds, shedding light on the evolving dynamics of financial markets. Our research deepens the field’s understanding of how diversification can optimize risk-adjusted returns, offering tactical insights for advancing portfolio management strategies and guiding future investment research.

This article has been tagged with: